%20(1).png)

Mixing Midterms and Markets

.png)

2022 has been an abnormal year in many ways, bucking many pre-COVID trends. The highest inflation readings in decades have pushed the Federal Reserve to take a more hawkish approach to its monetary policy, even if it means potentially driving the U.S. into recession. In the last couple of years, unprecedented stress has exposed cracks in our critical infrastructure and supply chains – the COVID-19 pandemic and Russia’s invasion of Ukraine to name a couple. Recently, Hurricane Ian tore through Florida and left destruction worth billions in damage. We know markets are fickle, and amidst these disruptions, they have quickly and efficiently priced in the ever-changing flow of news and information, leading to a steady decline in asset prices. While 2022 has been unusual, it has followed historical patterns in one unique area: midterm elections. Though November midterms have taken a backseat in the news cycle so far, markets have behaved in ways that show correlations to historical trends throughout history’s many midterm election years.

Midterm elections can produce heightened stress – the loudest voices often dominate the messaging with the more divisive and fearful prognosticators garnering the most attention. Mixing these ingredients creates a tenuous cocktail of worry, uncertainty, and political vitriol. With asset prices already in decline, what context can history provide as we shift into the meat of election season? While no one has a crystal ball, we can still explore trends and ideally help investors discern fact from fiction amidst all the noise and talking heads.

Midterm years are typically more volatile:

One popular Wall Street adage is that stocks hate uncertainty. Stock prices are created by investors – who ascribe value to a company by predicting its future earnings and cash flows and then discounting them back to today’s dollars. Markets are efficient, so when there is uncertainty surrounding politics and therefore the future environment for markets, stock prices can oscillate beyond historical norms.

Knowing midterms typically foment uncertainty, markets often respond with volatility. 2022 has been no different. One way to measure volatility is through standard deviation metrics; essentially these show the average distance between the mean and a data point in a specific data set. A high standard deviation represents more variance from the mean – and thus signifies volatility. Figure 1 displays the volatility spike we see during midterm years dating back to 1970. Here, you can see that midterm years have a median standard deviation of 15%, in contrast to the 13% in all other years. Another way to measure volatility is through drawdown metrics. Drawdown refers to the percentage an investment or index is down from its previous peak before it recovers. Figure 2 shows the average drawdowns of the S&P 500 during all four years of the presidential election cycle. Midterm years – year two – are noticeably lower than other years within the cycle at -19%. (Note the average performance coming out of the midterm elections – we’ll get to that here in a second)

Figure 1

Figure 2

Though 2022 has been unique with the breakout of war in Europe and a hawkish Federal Reserve battling inflation, we believe that analysis of drawdown percentages and standard deviations in midterm election years confirms that 2022 has seen volatility common within a midterm year.

Returns are typically muted during the election year, rise coming out of it

Uncertainty (there’s that word again) often comes with the territory during an election year. 2022 has seen many of the same questions asked during a typical election – will the President’s party lose seats in the Senate? House? And what will policy objectives look like if the President’s party maintains or loses control of Congress.

Markets tend to respond poorly to a cloudy outlook on the legislative front. While there are other factors at play, policymakers affect taxes and spending, which can then impact capital markets. Compared to non-election years, market returns tend to be more muted during the midterm election years as shown in Figure 3.

Figure 3

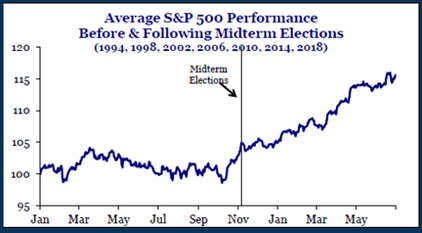

In addition, within those midterm election years, and in addition to the previously mentioned drawdowns, the S&P 500 returns are typically flat until the election wraps up. Figure 4 shows this trendline; once we reach November, stocks begin to price in a clearer economic agenda – whether it be gridlock or a flurry of new policy. Stocks generally respond favorably coming out of periods of uncertainty as well.

Figure 4

The Daily Policy Uncertainty Index[1] measures policy-related economic uncertainty through analysis of news, tax code and surveys of professional forecasters. Figure 5 shows the greater the level of uncertainty as measured by the index, the larger the returns as stocks begin to see more clarity across the political and economic realm.

Figure 5

Over the long run, markets are apolitical

We’ve all heard it before – the presumption that markets favor a certain political party over another, or that a particular candidate will be better for stocks. Be wary of pundits who proclaim to know exactly what will happen based on which party wins in November. Reality suggests that markets are indifferent when it comes to whether the elephant or the donkey holds the power. Figure 6 shows S&P 500 returns based on partisan control; it’s clear to us that the data shows no real correlation with returns.

Figure 6

Time in the market has historically been a more prudent strategy than timing the market; staying invested, anchoring your portfolio in the right areas, and allowing returns to compound has shown to reward investors who stay patient and disciplined. Figure 7 shows that stocks tend to rise overtime regardless of who is making decisions in D.C.

Figure 7

Conclusion

Though 2022 has been a particularly bumpy year as we exited a long bull market and period of low interest rates, markets have behaved similarly compared to other midterm years. Coming out of this period could also be bumpy - it is unusual to have a recession in the third year of a presidency[2], meaning the equity markets could be exploring uncharted waters in the coming months. We don’t have a crystal ball, but we can rely on trends and patterns to inform us: we believe you can expect volatility and muted returns through October and into November and that, ultimately, markets are politically indifferent.

[1] US Monthly Economic Policy Uncertainty Index

[2] Strategas, Post-Midterm Sector Trend Violates A Recession Playbook

Browse our collection of resources from trusted thought leaders.

Balentine experts offer their authentic take on the latest financial topics, including our exclusive market publications, news, community events, and more.

.png)

%20(1).png)