%20(1).png)

A Healthy Consolidation

.png)

“Rapidly rising or falling markets usually go further than you think.”

Bob Farrell, Market Rules to Remember

Markets have a way of challenging our instincts. After extended periods of strong performance, it is natural to assume that elevated valuations signal an imminent end. Yet history suggests otherwise. As Bob Farrell famously observed, “Rapidly rising or falling markets usually go further than you think.” Momentum, once established, is a powerful force. Trends that have persisted for long periods often continue longer than expected, even as they periodically pause to digest gains.

The fourth quarter of 2025 reflected this. Following a powerful advance earlier in the year, public markets experienced healthy consolidation rather than deterioration, allowing markets to absorb gains and reposition for what comes next. Returns moderated; leadership broadened, and some of the more speculative areas of the market cooled, while underlying fundamentals, particularly earnings growth, remained intact.

Private markets reflected a similar dynamic. As financing conditions have improved, activity has begun to reaccelerate from the slowdown that followed 2021, with capital gradually moving off the sidelines. Looking ahead, improving deal flow and an expected pickup in exit activity, including a stronger IPO environment in 2026, point to a market that is transitioning from retrenchment to renewed engagement.

Taken together, this backdrop suggests not an end to momentum, but a healthy consolidation across both public and private markets that strengthens the foundation for opportunity ahead. In this report, we reflect on performance across public and private markets in 2025, take a closer look at the fourth quarter, and share our thoughts on the opportunities and risks ahead in 2026.

Public Markets

Looking Back: 2025

In a year of high growth, markets experienced a healthy consolidation in Q4. 2025 was a powerful year in the markets, with MSCI ACWI's [1] 22.9% its best price return since 2019 and a strong S&P 500 return of 16.4%, its third straight double-digit year. Globally, 2025 was robust, with international stocks outperforming domestic stocks for the first time in many years. While the falling U.S. dollar was a factor here, the strength of economies in both Europe and Japan should not be dismissed; both regions are beginning to show signs of follow-through and confirmation of strength. Not surprisingly, the market remains optimistic, with most sentiment indicators pointing to a strongly bullish tilt. And make no mistake, investors have put their money where their mouths are, with record quarterly equity inflows of $400 billion. This wealth effect has carried over into consumer spending, which has remained on trend despite relatively weak consumer surveys.

Zooming in on Q4, the S&P 500 returned 2.3%. With a combined return of 19.2% in Q2 and Q3, it would be easy to view Q4 as a sign of market weakness; however, we believe the story is more nuanced. Following the shock of Liberation Day in Q1, [2] growth in Q2 & Q3 reflects a strong rebound, and Q4 served as a healthy pause, a moment for markets to consolidate the gains that occurred in 2025 — and set the groundwork for continued growth in 2026.

Some indicators of healthy consolidation include:

- Market Broadening. In Q4, the market shifted away from technology and into more cyclical sectors, increasing market breadth. This broadening into previously neglected sectors, such as Financials, Healthcare, Industrials, and Consumer Discretionary, is a condition generally necessary for the bull market to continue.

- Corrections in Frothy Areas of the Market & Continued Growth in Large-Cap Stocks. Cryptocurrencies and stocks with a higher volatility relative to the market fell. Meanwhile, Large Cap stocks fared better as S&P 500 earnings estimates continued to trend higher, and index-level margins returned to a record high. Helping the cause was the stability of Treasury yields, which defied analyst concerns that an inflation rebound might lead to higher interest rates that could derail any market strength.

Balentine’s 2025 Performance

Our relative results this year reflect shifting leadership in the stock market. Amidst these changes, we believe our data-driven, disciplined investment strategy protects wealth and compounds it over time. In the first quarter, our strategies lagged benchmarks as international equities outperformed and our positioning remained more U.S.-centric. In the second quarter, we added exposure to developed international markets. At the same time, growth stocks, which struggled in April, rebounded strongly into June and provided an additional tailwind to our strategies. In the third quarter, we reallocated a portion of domestic Large Cap Core Equities into Emerging Markets as momentum accelerated, and capital rotation into the region gained strength. In the fourth quarter, we increased our overall weight to equities, which served us well as equities outperformed bonds during the quarter.

Recall that a cornerstone of our investment process is maintaining discipline and diversifying between short-term tactical opportunities and long-term alpha drivers, even in markets where returns are heavily concentrated in specific themes and in a small group of companies. To achieve this, we incorporate factor strategies grounded in fundamentals like profitability and broader economic measures such as Leading Economic Indicators. While cap-weighted indices can perform well during momentum-driven rallies, history shows that nontraditional weighting methodologies like factor investing can add value once market leadership shifts or concentration eases. This discipline reflects our philosophy: we believe prudent diversification and thoughtful construction are essential to protecting and compounding wealth over time.

Looking Ahead: 2026

Here are our key themes and chief concerns. As we look forward to 2026 and ponder both the quantitative and qualitative possibilities, we note that the strength during 2025 was less about speculative activity and more about the robust earnings growth stocks exhibited during the year, underscoring the strength of the U.S. economy. However, the market has not gone up for four consecutive years since before the Global Financial Crisis (GFC). As we enter the fourth year of market strength, we identify key market & economic themes as well as potential concerns.

Key Market & Economic Themes for 2026

- A New Fed Chairman will be appointed in 2026. This person will likely be more dovish than Jerome Powell, raising the question: How will the new Fed Chairman continue to navigate the tightrope between inflation concerns and employment concerns?

- Tax breaks from One Big Beautiful Bill [3] will stimulate the economy.

- A robust pipeline of initial public offerings (IPOs) foreshadows a strong year ahead for capital markets in 2026.

- When AI technology entered the market, companies developing it experienced significant growth, which has driven the growth of the S&P 500. In 2026, sectors of the market implementing AI in their company operations will continue to “catch up” on growth and innovation.

Potential Concerns for 2026

Some of 2025’s key growth drivers could become concerns in 2026.

Valuations Outpacing Earnings Could Lead To Multiple Contraction

As we enter 2026, we would not suggest yet that risks facing equity investors are above average for this cycle. However, valuations remain elevated, albeit not yet at extreme levels. Of course, valuations were elevated last year at this time, and the market went up because earnings came through. If earnings do not keep up, the market could begin to doubt the sustainability of the AI productivity improvement story. Equities frequently react negatively when fundamentals fail to keep pace, with equities being particularly sensitive when valuations are rich. This could create multiple contraction on top of any earnings shortfall.

Concentrated Market Sentiment May Result in a Bullish Pause

As referenced earlier, market sentiment ended the year with a strongly bullish tilt, which was expressed primarily (though not exclusively) in the more expensive corners of the market. The silver lining here is that there are many pockets of the market with relatively restrained sentiment, albeit at a lower market cap weighting than that of the more expensive corners. So, while any pullback in sentiment is likely to have an effect on the overall market given the market concentration at the top, such sentiment pullback is unlikely to affect the entire market as a whole, which would be a bullish pause for the market as a whole, but would possibly not come without some pain to parts of the market.

A New Fed Chair Could Create Increased Inflation

With the likely appointment of a new Federal Reserve Chairman this May, we are likely to see someone more dovish, in line with President Donald Trump’s preferences — now, what does that mean? After the December cut, the Fed Funds target range is 3.50-3.75%, and Trump has repeatedly said that the Fed should instantly lower the Fed Funds rate by a full percentage point and follow up with several more cuts (without being overly specific). Were the Fed to cut the Fed Funds rate by at least another 125 bps, in addition to the 25 bps delivered in December, there is a not-insignificant chance that inflation returns, especially given the strong Q3 2025 real GDP print of 4.3%. Much of the inflation outlook will also depend on how quickly the labor market continues to slow and how much productivity gains we see from AI and other associated technologies. But the possibility that we quickly go from tight monetary policy to neutral monetary policy to loose monetary policy should not be dismissed.

An important historical note: When rate cuts occur at or near market all-time highs, both equity and bond markets tend to perform well during the following 12 months. So, absent a recession, proactive cuts can help prevent the economy from tipping into contraction, which as we have mentioned, is quite different from the reactive cuts that typically come after a downturn has already begun. We are not overly concerned about a severe resurgence of inflation, but it is worth monitoring.

Private Markets

At Balentine, we take a thoughtful, long-term approach to private capital that’s built around our clients. We seek out areas of the market that we believe are well-positioned to perform and partner with experienced managers to provide our clients with access to high-quality opportunities. From there, we build custom portfolios that reflect each client’s goals, time horizon, and need for flexibility. As our clients’ wealth grows, we help them grow with it — expanding exposure, simplifying the process, and staying focused on what matters most to their families’ futures.

In Q4, private markets continued to offer compelling opportunities as capital markets adjusted to higher-for-longer interest rates and selective dislocations. We remained focused on partnering with experienced managers and accessing strategies that combine attractive return potential with disciplined downside protection.

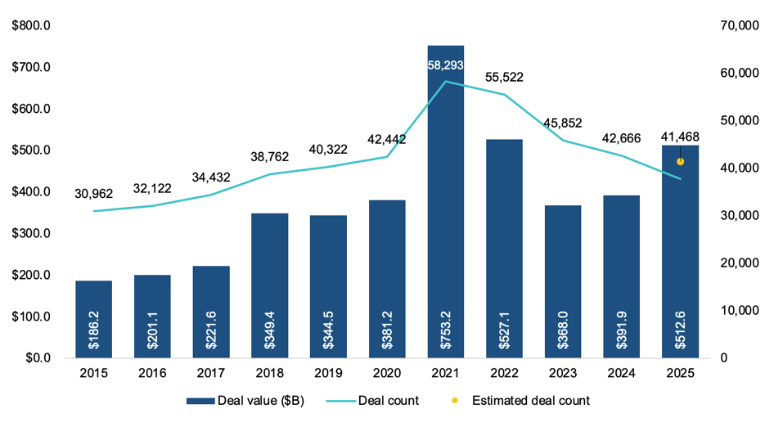

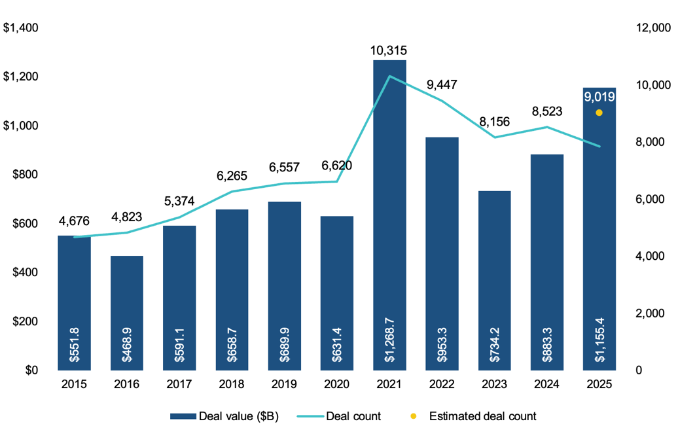

Looking ahead to 2026, after a multi-year slowdown beginning in 2021, private market deal activity is rebuilding momentum as interest rates have come down and financing conditions have improved. With more transactions being completed and a strong IPO calendar expected in 2026, capital that stepped aside earlier in the cycle appears to be re-entering the market (Figure 1).

FIGURE 1: U.S. Private Capital Deal Activity (2015-2025)

2025 had the most private equity and venture capital deals since 2021, evidence that private market deal activity is rebuilding momentum as interest rates have come down and financing conditions have improved.

Private Equity Deal Activity (2021 - 2025)

Venture Capital Deal Activity (2021-2025)

Here’s What’s New In Private Capital:

Open Funds

There are Four Funds Open for Investment. If any of these opportunities are a fit for your portfolio, your Relationship Manager will be in touch.

- NEW: Magnolia Growth and Innovation II: invests in early-stage and growth companies at the forefront of innovation

- NEW: Redwood Buyout Opportunities II: invests in established businesses, using operational improvements and strategic repositioning to create value

- Private Credit Opportunities II: invests in diversified exposure to private credit by emphasizing senior secured lending, credit secondaries, and opportunistic lending in a higher-rate environment

- Sun Belt Plus Real Estate Opportunities I: invests in private real assets with an emphasis on real estate credit, workforce housing, and digital infrastructure in high-growth Sun Belt markets.

Impact Spotlight: In Q4, client investment supported access to affordable housing in the United States. Through Sun Belt Plus Real Estate Opportunities I, we allocated funds to Infinity RE Impact IV, which refurbishes Section 8 housing. The refurbished homes have higher rent, and with support from HUD, this increase is covered so folks have better living at the same cost.

Closed Funds

There are Four Closed Funds: Decarbonization 2022, Industrial & Aerospace 2022, Logistics 2022 & Credit Opportunities 2023. This quarter, we’ll highlight Decarbonization 2022. For more information on our funds and performance reporting, reach out to your Relationship Manager.

Decarbonization 2022 seeks to fund opportunities that benefit from the global transition toward a lower-carbon economy, with a focus on infrastructure, renewable energy, and decarbonization.

Impact Spotlight: In Q4, our clients helped to create 8 million kWh of clean energy – enough to power 10,500 homes annually. How? Our Fund Manager, Kendall, builds small-scale solar farms. Recently, they reached 21 MW of operational solar power with another 16–20 MW coming online shortly.

Opportunistic Investments

This quarter, we’re highlighting CAZ Touchdown Fund. Through CAZ, our clients invested in Paris Saint-Germain (PSG), one of the world’s most recognized global soccer franchises. The investment was made as part of the fund’s flexible allocation, which allows up to 20% of capital to be invested across a broad range of professional sports opportunities.

This investment is focused on supporting PSG’s continued brand expansion in the United States and other international markets, leveraging the club’s global fan base, commercial partnerships, and growing presence in North America ahead of major international soccer events. The strategy reflects our broader approach within CAZ Touchdown of targeting high-quality sports assets with durable brands, diversified revenue streams, and long-term global growth potential.

Closing Perspective

For investors, the current environment presents both opportunities and challenges. Resilient economic growth, ongoing technological innovation, and supportive policy provide strong reasons for optimism in 2026. At the same time, periods of transition, including the equity market rotation seen in recent months, can bring volatility and test conviction.

We believe artificial intelligence will remain a defining force for years to come. As attention potentially shifts from the builders of AI to the companies applying it to drive revenue and margins, selectivity will matter.[4] At the same time, our Private Capital strategies continue to provide essential diversification, offering opportunities in credit, real assets, and early-stage growth that complement public market exposure.

Periods of transformation demand both optimism and discipline. That is why our approach continues to emphasize diversification, careful manager selection, and a long-term perspective. We believe these principles remain the best foundation for protecting capital and capturing opportunity in the years ahead.

Thank you for the continued trust you place in our team and process. We welcome your questions at any time and look forward to guiding you through the opportunities ahead.

Sincerely,

David Damiani, CFA

Chief Investment Officer

References & Further Reading

[1] The MSCI World Index is a free float-adjusted market capitalization-weighted index that is designed to measure the equity market performance of developed markets. The MSCI World Index consists of the following 23 developed market country indices: Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, the United Kingdom, the United States.

[2] Tariffs Are Here (Investment Strategy Team, Balentine)

[3] OBBBA and Your Portfolio: Four Key Shifts (Susie Wang, CFA, SCR, Balentine)

[4] Read more about AI's impact and the themes that will shape markets for years to come in Finding Clarity (Susie Wang, CFA, SCR, Balentine), the first article of our 2026 Capital Markets Forecast.

Disclosures

The views expressed represent the opinion of Balentine LLC (“Balentine”). The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Balentine believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Balentine’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance, or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. International investments may involve risk of capital loss from unfavorable fluctuation in currency values, from differences in generally accepted accounting principles, or from economic or political instability in other nations.

The investments highlighted were selected for illustrative purposes only and do not represent the full range of securities bought, sold, or recommended for clients during the period shown.

Past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by Balentine or any non-investment related services) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. The information provided in this report should not be considered financial advice or a recommendation to buy, sell, or hold any particular security. There is no assurance that any securities discussed herein will remain in an account’s portfolio at the time you receive this report or that securities sold have not been repurchased.

This is not an offer to sell, or a solicitation of an offer to purchase, any fund managed by the Adviser. Such an offer will be made only by an Offering Memorandum, a copy of which is available to qualifying potential investors upon request.

Chartered Financial Analyst® (CFA®) designations are licensed by the CFA® Institute to use the CFA® mark. CFA® certification requirements: Hold a bachelor’s degree from an accredited institution or have equivalent education or work experience, successful completion of all three exam levels of the CFA® Program, have 48 months of acceptable professional work experience in the investment decision-making process, and fulfill society requirements, which vary by society. Unless upgrading from affiliate membership, all societies require two sponsor statements as part of each application; these are submitted online by sponsors.

Balentine LLC (“Balentine”) is an investment adviser registered with the U.S. Securities and Exchange Commission. Registration does not imply endorsement or training. More information about Balentine’s investment advisory services can be found in its Form ADV Part 2, which is available upon request.

Browse our collection of resources from trusted thought leaders.

Balentine experts offer their authentic take on the latest financial topics, including our exclusive market publications, news, community events, and more.

.png)

Don’t Mistake Wealth for Legacy

You Sold the Company, Now What?

.jpg)

%20(1).png)