%20(1).png)

Tariffs Are Here

.png)

It’s been more than four months since “Liberation Day,” when President Donald Trump announced across-the-board tariffs on imports beginning August 1. On the other side of this deadline, here are our key takeaways:

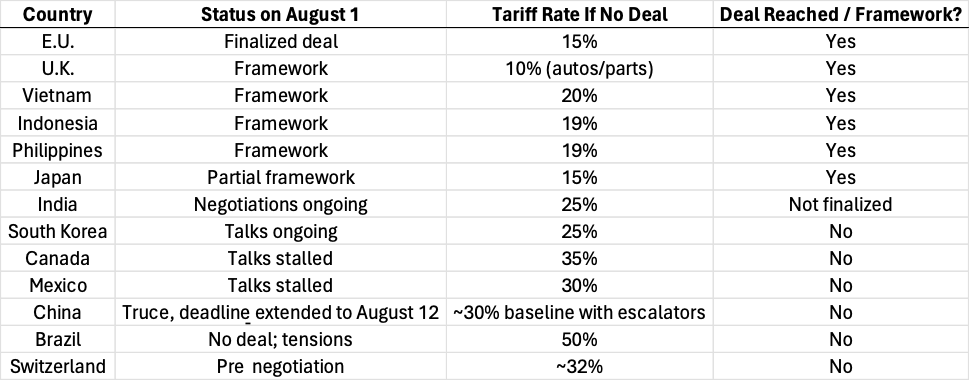

- Countries that already have free trade agreement structures in place with the U.S. even if they have not yet been formalized, have avoided the steepest tariffs. At the time of writing, examples include the E.U,1 U.K., Japan, South Korea, Indonesia, Vietnam, and the Philippines.

- Countries without trade agreements in place will have steep ad valorem rates,2 in some cases up to 50%. Given the agreements that have been reached so far, it will likely be harder for these countries to get deals as good as the countries that have already agreed to framework trade agreements.

- Having said that, Treasury Secretary Scott Bessent continues to emphasize that though tariffs started on August 1st, the U.S. will commence or continue negotiations with countries with whom it doesn’t already have a deal.

- Though President Trump has softened his stance on tariffs since mid-April, and despite the market’s approval this pivot, we expect the path will be volatile throughout the negotiation process in line with the President’s “Art of the Deal” approach. While we do not expect markets to experience anything near what they experienced in April, it would not surprise us if August’s markets demonstrate a step up in volatility relative to that of May-July, around the honing of specifics within the deals.

Where Tariffs Stand Today

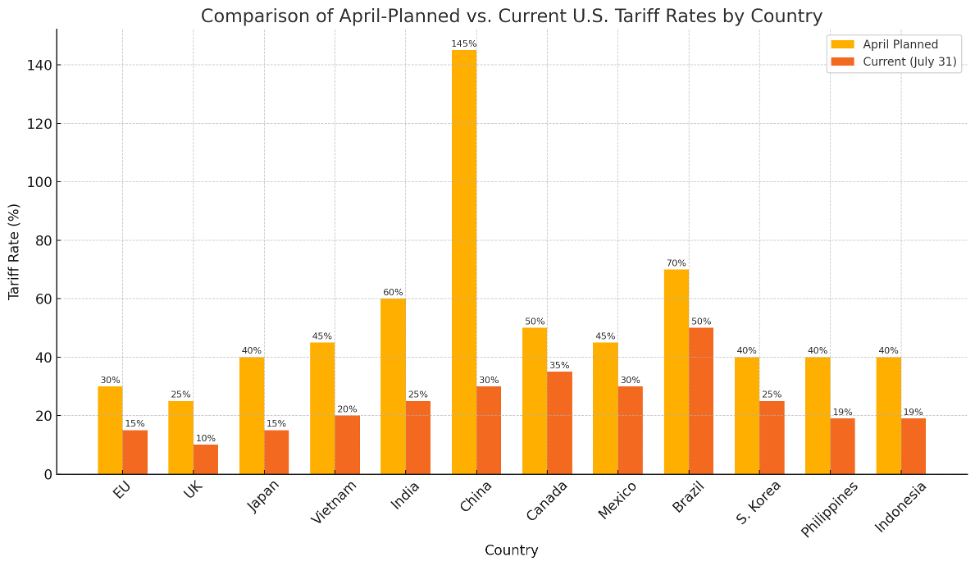

Here’s where tariffs stood on April 2 – and where they stand today.

FIGURE 1: Where Tariffs Stand Today, sorted by type of good

FIGURE 2: How Tariffs Will Impact Major Economies of North America, sorted by status on August 1

Where goods overlap between Figures 1 and 2, Figure 2 tariffs are additive. So, for example, if no deal is reached with Indonesia, tariffs on auto parts will be levied at 44% (25% + 19%).

Within North America, talks have stalled with Mexico and Canada on renegotiation of the United States-Mexico-Canada Agreement(USMCA). Figure 2 shows that Canada and Mexico have rates of 35% and 30% respectively on goods not in compliance with the USMCA.

Additional Developments:Tax Policy and Deregulation

Beyond President Trump’s softened tone since the Liberation Day rollout, there is another aspect that bears noting. In early July, "One Big Beautiful Bill" was passed, and we believe some clauses within it make OBBBA a game changer for the tariff regime and will likely ameliorate much of the concern about tariffs, for example:

- Tariff Exemptions: Countries can negotiate preferential access to the U.S. market through individual bilateral agreements. These agreements would typically reduce the 10% baseline tariff and sector-specific tariffs (e.g., autos and auto parts, metals, etc.) in exchange for strategic investment in the U.S. or strategic cooperation such as military basing and energy purchase. This structure replaces a one-size-fits-all model, tailoring the biggest benefits to our allies.

- “Tariff Credits” for U.S. Exporters: U.S. exporters who face retaliatory tariffs abroad can receive federal tax credits or rebates tied to lost revenue. This will help cushion sectors such as agriculture and aerospace that suffer from foreign counter-tariffs, with the aim of stabilizing crucial U.S. industries during trade disputes.

- Incentives for Supply Chain Repatriation: Tax breaks and federal financing are available for reshoring or “friendshoring”3 production, with the long-term goal of reducing vulnerability to foreign retaliation or other sources of supply chain disruption such as that experienced during the COVID-19 pandemic. Crucial sectors prioritized here include semiconductors, autos, minerals, and defense manufacturing.

- Appeals Process and Sunset Clauses: Trade agreements include clauses that allow countries to reassess fairness and compliance within 3-5 years. This provides a framework for adjusting tariffs down the road, as appropriate, which should make for more effective trade planning and investment. Additionally, countries signing trade agreements will have the ability to appeal their tariffs to a review board to make a case that their remaining tariffs should be adjusted based on any facts they feel were not contemplated when the tariff was assessed.

- Allowance of Bloc Trade Agreements: Countries can “bloc” together to negotiate as a group to give themselves better terms (e.g., ASEAN). This has already come to pass, as The Philippines, Indonesia, and Vietnam negotiated a Pacific agreement that led to tariffs being capped at only 15%-20%. This balances coordination among regions with like-minded goals while refraining from a World Trade Organization-type multilateral approach.

We believe these aspects of OBBBA have improved the tariff situation by bringing more certainty to tariff outcomes for countries that negotiate a deal, locking in preferential bilateral terms for partner countries while also allowing structured access to emerging economies in exchange for regional investment. By codifying tariff levels via formal executive actions and trade letters, OBBBA brings clarity to businesses after much confusion and a seemingly helter-skelter approach initially.

In Closing

More than four months after “Liberation Day,” the tariff landscape has begun to take shape. Countries with early trade agreements—like the EU, U.K., Japan, and parts of Southeast Asia—have avoided the harshest tariffs, while others face steep rates of up to 50%. Though negotiations continue, we believe markets should brace for some volatility as deal terms are refined. Within North America, talks with Canada and Mexico have stalled, and goods noncompliant with the USMCA now face 30–35% tariffs.

At the same time, the passage of OBBBA has reshaped the outlook. It gives countries a way to earn reduced tariffs through specific agreements tied to U.S. interests, offers tax credits to help U.S. exporters facing retaliation, and encourages companies to bring critical supply chains back home. It also allows countries to appeal tariffs and negotiate in blocs—steps that offer more flexibility without sacrificing national priorities. While uncertainty remains, these changes suggest a more focused and adaptive approach to trade—one that balances protection with partnership and provides clearer paths forward for businesses and policymakers alike.

We continue to monitor developments closely and will adjust portfolios only when necessary and prudent. In the meantime, we encourage you to stay focused on your long-term goals and trust our unemotional, data-driven process. Please don’t hesitate to reach out if you have any questions or would like to discuss your portfolio in more detail. We're here for you.

1The European Union acts as one negotiating body for all member countries.

2Ad valorem taxes, Latin for “according to the value,” are based on the value of the item being taxed.

3"Friendshoring” refers to moving production to countries with whom we have amicable relationships, where we don’t have to worry that a geopolitical problem will put us in a bind, like during the COVID-19 pandemic.

Browse our collection of resources from trusted thought leaders.

Balentine experts offer their authentic take on the latest financial topics, including our exclusive market publications, news, community events, and more.

.png)

The Tax-Aware Investor

Beyond the Exit: How Opportunity Zones Turn a Tax Bill Into a Long-Term Investment

%20(1).png)